Products You May Like

Topline Preliminary Estimates

- 10-Year Revenue (Billions) +$1,325

- Long-run GDP -0.2%

- Long-Run Wages +0.6%

- Long-Run FTE Jobs -387,000

Tax Foundation General Equilibrium Model, September 2024

Former President Donald Trump has not released a fully detailed taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

plan as part of his current bid for reelection, but he has floated several tax policy ideas. Among various (sometimes competing) ideas, he seeks to extend the expiring 2017 Tax Cuts and Jobs Act (TCJA) changes, further reduce the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

rate in some form, exempt tips and Social Security benefits from tax, impose a 10 percent or higher universal baseline tariff on all imports, and raise current tariffs on China to at least 60 percent. He has also discussed replacing the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

with tariffs.

The impact of Trump’s proposals will vary significantly depending on which combination of policies are pursued. The economic effects could range from slightly positive to slightly negative, while the revenue effect ranges across deficit increases of different magnitudes. As with any economic model, ours does not capture all the possible effects of the proposed tax and tariffTariffs are taxes imposed by one country on goods or services imported from another country. Tariffs are trade barriers that raise prices and reduce available quantities of goods and services for U.S. businesses and consumers.

policies, such as changes in compliance costs, the geopolitical implications of further trade wars, the impact of different tax burdens on different sectors and types of investments, or how uncertainty affects economic decision-making.

Our estimates illustrate that Trump’s proposed tariffs threaten to offset the economic benefits of his proposed tax policy changes, while falling short of offsetting the tax revenue losses. Trump’s combination of policies could therefore shrink economic output and grow the national debt.

Modeling the Major Provisions Proposed by Candidate Trump

Because Trump has suggested various ranges for his proposed tax and tariff policies, we have estimated a range of potential economic and revenue effects based on the different policies he has discussed.

For tax policy, we model the following major proposals:

- Permanence for the expiring individual provisions of the TCJA

- Permanence for the expiring estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs.

provisions of the TCJA - Permanence for the business tax phaseouts of the TCJA (100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

, R&D expensing, and an EBITDA-based interest limitation) - Lowering the corporate tax rate to 20 percent

- Lowering the corporate tax rate to 15 percent

- Exempting tips from income taxes

- Exempting Social Security benefits from income taxes

- Eliminating the green energy subsidies in the InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

Reduction Act

For tariff policy, we model the following major proposals:

- Raising current Section 301 tariffs on China to 60 percent

- Imposing a universal tariff on all US imports of 10 percent

- Foreign retaliation on US exports, in-kind, matching the 60 percent and 10 percent tariffs

- Imposing a universal tariff on all US imports of 20 percent

Note that we do not model Trump’s recent proposal that would restrict the 15 percent corporate tax rate to a subset of firms engaged only in domestic production, as it lacks specifics; doing so would reduce the economic and revenue effects of the policy. We also exclude from our analysis the idea floated by vice presidential candidate Sen. JD Vance to increase the child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

to $5,000.

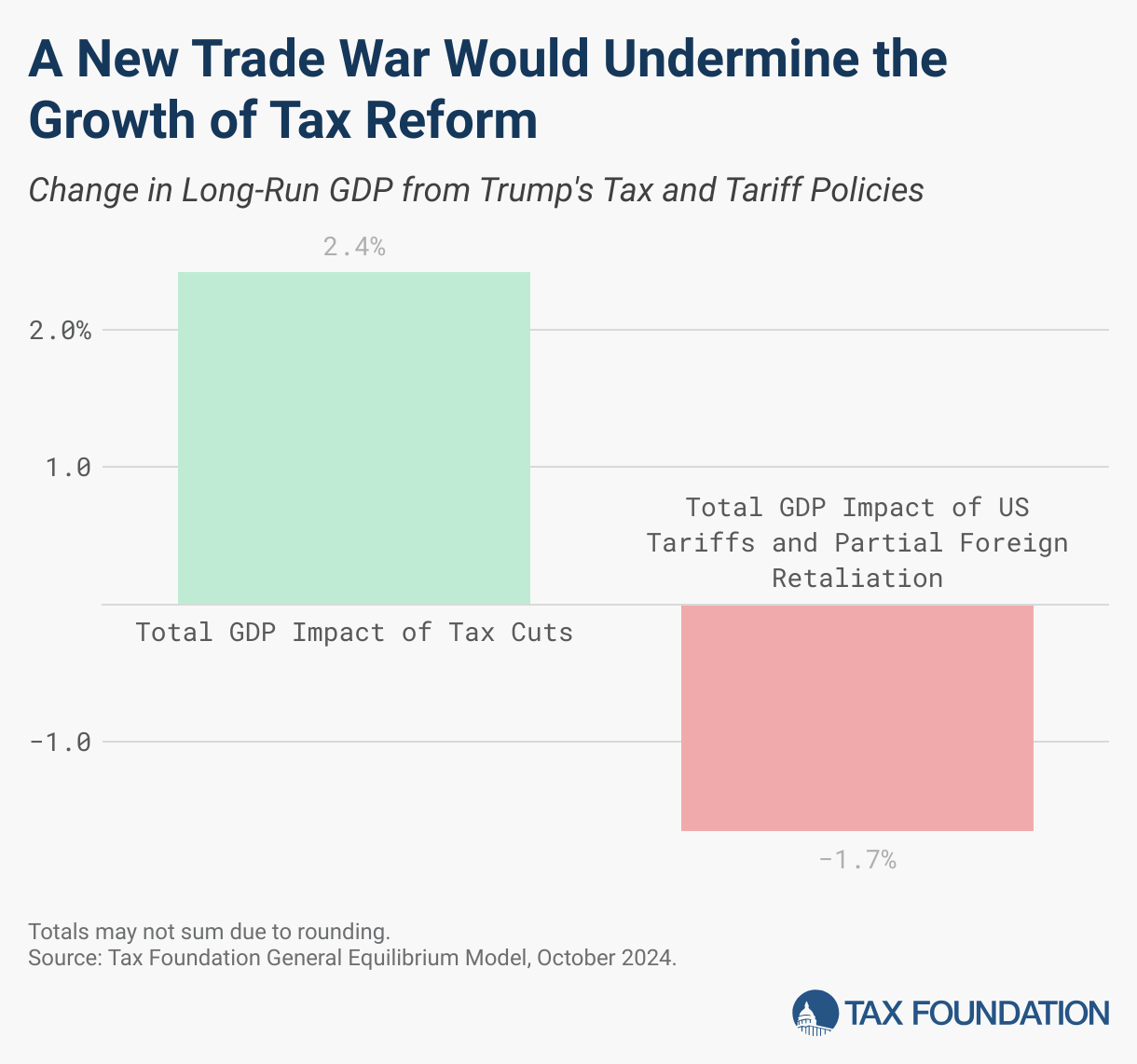

Using the Tax Foundation’s General Equilibrium Model, we estimate the major tax changes proposed by Trump would increase long-run GDP by about 1.5 percent. Permanence for the individual, estate, and business tax components of the TCJA are the largest drivers, together increasing long-run GDP by 1.1 percent; lowering the corporate tax rate to 20 percent (+0.1 percent GDP), further lowering it to 15 percent (another +0.3 percent GDP), and exempting Social Security and tips from income tax (+0.1 percent of GDP), make up the remainder. We estimate that repealing the green energy tax credits has no long-run effect on GDP because the policies are scheduled to expire.

The gross tax cuts would decrease federal tax revenue over the 10-year budget window by $6.1 trillion on a conventional basis and by $5.3 trillion on a dynamic basis. Repealing the IRA green energy tax credits would increase revenue by $921 billion, resulting in a net revenue impact from tax policies that would decrease federal tax revenue by $5.2 trillion on a conventional basis and by $4.4 trillion on a dynamic basis.

We estimate the proposed tariffs of 60 percent on China and an additional 10 percent on all imports would reduce long-run GDP by nearly 0.8 percent. Further lifting the 10 percent tariff to 20 percent would take the combined economic effect of the tariff proposals to a 1.3 percent drop in long-run output.

To illustrate the potential harms from foreign retaliation, we estimate the impact of a 10 percent tariff on all goods exports plus additional in-kind retaliation on US goods exports to China. We estimate that combination would reduce US GDP by an additional 0.4 percent in the long run while raising no additional revenue for the US government.

We estimate the 10 percent universal tariff would raise about $2 trillion over 10 years, while the increased tariffs on China would raise about $560 billion. Lifting the universal tariffs to 20 percent would raise almost $1.3 trillion in additional revenue. The total revenue increase from tariffs ranges from $2.6 trillion to $3.8 trillion on a conventional basis and from $2.1 trillion to $3.1 trillion on a dynamic basis, factoring in foreign retaliation as well.

Altogether, we estimate the combination of proposed tax and tariff changes, including foreign retaliation, would reduce long-run GDP by nearly 0.2 percent and hours worked by 387,000 full-time equivalent jobs. Both the capital stock and wages would still rise—by 0.3 percent and 0.6 percent, respectively—as the better treatment of capital investment from permanence for 100 percent bonus deprecation and R&D expensing dominates those economic channels. Depending on which combination of proposals Trump ultimately pursues, the overall impact on GDP could range from slightly positive to slightly negative for the US economy.

Under the full suite of tariffs and IRA repeal, we estimate the deficit would rise by $1.3 trillion over the next decade on a conventional basis. After accounting for economic impacts, we estimate the deficit would rise by $1.2 trillion over the next decade. The increase in the budget deficit would lead to higher interest payments made to foreigners, resulting in a reduction in American income (GNP) of 0.2 percent, driving a wedge between the effect on American output and American incomes. The extent to which the budget deficit rises hinges on the exact combination of proposals, and a larger deficit increase would result in a larger decrease in American income.

We estimate that on both a conventional and dynamic basis, debt-to-GDP would rise under the combination of policies proposed by Trump. On a conventional basis, it would rise by 10.6 percentage points and on a dynamic basis, by 9.4 percentage points.

Overall, Trump’s policies would reduce distortions in one part of the tax system, namely income taxes, only to replace them with new distortions in another part of the tax system, namely tariffs. The combination of policies under consideration risks shrinking the economy and growing the debt.

Modeling Notes

We assume TCJA permanence entails the following changes, described here in our recent publication:

- Lower rates and reconfigured brackets

- Larger standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes.

- Eliminated personal exemption

- Larger child tax credit

- Limited itemized deductions, including for state and local taxes paid, home mortgage interest, and miscellaneous

- Eliminated Pease limitation

- Larger AMT exemption and exemption phaseout thresholds

- 20 percent deduction for pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates.

income and limitation on noncorporate losses - Larger estate tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax.

- 100 percent bonus depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment.

- Expensing for research and development

- Deduction for net interest limitation based on EBITDA

To model the economic effects of tariffs, we treat them as an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections.

applied to US imports. As an excise tax, tariffs create a wedge between the price a consumer pays and the price a producer receives. In Tax Foundation’s modeling, we hold the price level constant, passing tariffs back to the factors of production. In other words, tariffs reduce the amount of revenue businesses have to compensate their workers and shareholders, resulting in a reduction in real incomes.

To model the revenue effects of US-imposed tariffs, we first take the affected imports based on 2023 levels multiplied by the inclusive tariff rate (consistent with the revenue estimating convention that the price level remains constant). We then apply a noncompliance rate of 15 percent, based on the average tax gapThe tax gap is the difference between taxes legally owed and taxes collected. The gross tax gap in the U.S. accounts for at least 1 billion in lost revenue each year, according to the latest estimate by the IRS (2011 to 2013), suggesting a voluntary taxpayer compliance rate of 83.6 percent. The net tax gap is calculated by subtracting late tax collections from the gross tax gap: from 2011 to 2013, the average net gap was around 1 billion.

, an elasticity of import demand with respect to price of -0.997, and income and payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue.

offsets of approximately 27 percent to 29 percent. On a dynamic basis, revenue falls further as tariffs result in a reduction in real incomes and output.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share