Products You May Like

Key Findings

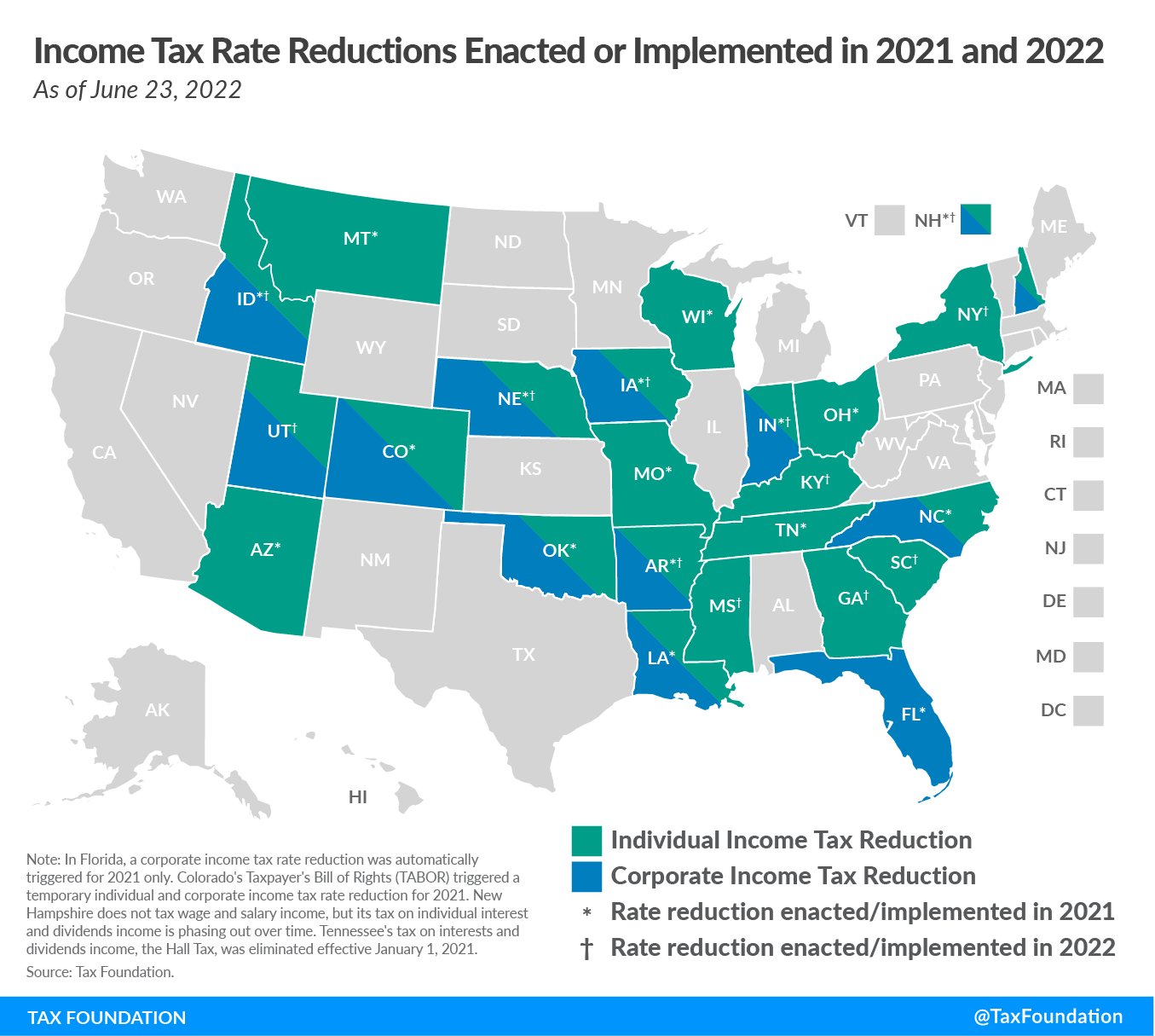

- Over the past two years, a wave of tax reform has swept the country, with a historic number of states improving their tax competitiveness by reducing income tax rates and enacting flatter structures.

- Since 2019, Wisconsin has made improvements to its three lowest marginal individual income tax rates, but its top marginal rate of 7.65 percent remains among the highest in the country.

- A new era of increased remote work flexibility is contributing to states’ decisions to reduce income tax rates, and states that stand still risk falling behind their peers.

- Wisconsin’s state sales tax rate is among the lowest in the country, and the sales tax base excludes many consumer services.

- Numerous economic studies show corporate and individual income taxes are more harmful to economic growth than are consumption taxes.

- Given Wisconsin’s strong budget surplus and continued projected revenue growth, policymakers have a solid opportunity to rebalance Wisconsin’s tax structure by shifting reliance away from economically harmful taxes on productivity and toward less harmful taxes on consumption.

- This report offers five sample comprehensive tax reform options to enhance Wisconsin’s tax competitiveness with a focus on reducing economically harmful taxes on labor and investment.

Table of Contents

Introduction

Over the past two years, a wave of tax reform has swept the country, with a historic number of states enacting laws to improve tax competitiveness. In 2021, Wisconsin was among 13 states to enact laws reducing individual or corporate income tax rates, and as of this writing, 11 states have enacted legislation in 2022 to reduce income tax rates. Six of these tax-cutting states sit within a 200-mile radius of Wisconsin, creating an intensely competitive regional tax environment.

In 2019, 2020, and 2021, Wisconsin reduced its second-highest individual income tax rate once and its lowest two rates twice, targeting tax relief toward low- and middle-income taxpayers. But Wisconsin’s top marginal individual income tax rate—which applies to approximately two-thirds of pass-through business income—has been left unchanged for a decade, and the state income tax landscape has grown dramatically more competitive during that time. In fact, 25 states have lower top marginal individual income tax rates now than they did in 2012.[1] As of 2023, when Iowa’s top rate drops to 6 percent (with further reductions to 3.9 percent),[2] Minnesota and Wisconsin will be left with the highest top marginal individual income tax rates of all the non-coastal states stretching from California to New York.[3]

Adding to the urgency of reform, the COVID-19 pandemic quickly accelerated a trend toward more flexible workplace arrangements, and many workers now find themselves free to live in a state of their choosing while working for an employer in another. With enhanced workplace flexibility and with inflation at its highest level in four decades, many people are leaving high-tax, high cost-of-living jurisdictions in favor of states with lower costs of living, including lower taxes—specifically, states with low or no income taxes.

Individuals and businesses weigh many factors when deciding where to locate or invest—such as family and weather, as well as infrastructure, quality of life, and a suitable workforce. Not many of these factors are within policymakers’ control, and, even when they are, economic growth generated from educational improvements or infrastructure investments, for example, may take years to manifest. But tax policy is within policymakers’ control, and policy changes can yield real economic results much more quickly.

Even with the improvements Wisconsin has made since 2019, the state is quickly falling behind on income tax competitiveness, and this has implications both for business investment and for Wisconsin’s ability to attract and retain a highly skilled workforce.

This publication presents five sample comprehensive tax reform options for Wisconsin and explains how each of the proposed policy changes would help Wisconsin become more economically competitive. Several components of these sample tax reform options are similar to the components of the reform options that were presented in our 2019 publication Wisconsin Tax Options: A Guide to Fair, Simple, Pro-Growth Reform,[4] but these new options reflect current tax collections and revenue forecasts, as well as recent tax policy changes in Wisconsin.

An Overview of Wisconsin’s Tax Structure

The Tax Foundation’s State Business Tax Climate Index, published annually, evaluates states according to the competitiveness of their tax structures. In the 2022 edition of the Index, which is based on a snapshot of policies in place on July 1, 2021, Wisconsin ranks 27th overall, slightly below average.[5] Wisconsin’s scores on the individual, corporate, and unemployment insurance tax components drag down its overall score, but the state performs in the top 10 on sales and excise taxes and among the top 20 on property and wealth taxes. Table 1 shows Wisconsin’s 2022 Index rankings and how they have changed since the 2019 version of the Index,[6] which was referenced in our February 2019 publication Wisconsin Tax Options: A Guide to Fair, Simple, Pro-Growth Reform.

Wisconsin’s recent individual income tax rate reductions contributed to its improvement on the individual tax component, and reductions in property tax collections per capita and property taxes as a percentage of personal income contributed to its improvement on the property and wealth tax component.

Since unemployment insurance (UI) tax systems are similar in every state, a small change in one state’s policies can change its UI tax component ranking dramatically. Rates, meanwhile, fluctuated considerably from state to state during the pandemic. This explains the large improvement in Wisconsin’s UI tax ranking that occurred due to minor taxpayer-friendly improvements in the state’s UI tax structure combined with significantly higher rate schedules in some peer states.

| Component | 2019 Rankings (Backcast) | 2022 Rankings | Change |

|---|---|---|---|

| Overall Ranking | 33 | 27 | +6 |

| Corporate Taxes | 31 | 31 | — |

| Individual Taxes | 39 | 37 | +2 |

| Sales and Excise Taxes | 7 | 7 | — |

| Property and Wealth Taxes | 20 | 16 | +4 |

| Unemployment Insurance Taxes | 40 | 28 | +12 |

|

Note: The State Business Tax Climate Index measures how each state’s tax laws affect economic performance. A rank of 1 means the state’s tax system is more favorable for business; a rank of 50 means the state’s tax system is less favorable for business. Some 2019 rankings referenced here differ from rankings as originally published in the 2019 Index due to enactment of retroactive statutes and backcasting of methodological changes. Source: Tax Foundation, 2022 State Business Tax Climate Index. |

|||

Sample Tax Reform Options for Wisconsin

Our February 2019 publication Wisconsin Tax Options: A Guide to Fair, Simple, Pro-Growth Reform presented a menu of four comprehensive tax reform options for the state. All four options were approximately revenue neutral based on the revenue estimates and other data that were available at the time. Much has changed, though—in our world, in state tax policy, and even in Wisconsin’s tax code—over the past three years. Following the U.S. Supreme Court’s decision in South Dakota v. Wayfair, the state enacted a law requiring remote sellers and marketplace facilitators with more than $100,000 in sales into Wisconsin to collect Wisconsin’s state and local sales taxes. This resulted in an influx in sales tax revenue, which Wisconsin used to permanently reduce, on two separate occasions, the two lowest marginal individual income tax rates.

Wisconsin’s policy of collecting sales taxes from remote sellers proved fortuitous during the COVID-19 pandemic, when a great deal of consumption shifted online. Then, like most states, Wisconsin experienced strong own-source revenue growth in fiscal years (FYs) 2020-21 and 2021-22 and was one of 13 states to enact laws in 2021 reducing income tax rates.

In light of these changes, we chose to publish updated tax reform options that take into account the aforementioned changes to Wisconsin’s tax code and to the state tax landscape, as well as the most up-to-date Wisconsin tax collections figures and revenue projections. Several of the reform options we present in the pages to follow are similar to the options presented in our 2019 report, with some variations. Most notably, the updated options prioritize highlighting ways Wisconsin could move from a graduated-rate to a flat individual income tax, as four states have enacted laws to do since July 2021.

Given that Wisconsin is projected to close out the FY 2021-23 biennium with a budget surplus of $3.8 billion,[7] and given that the state is projecting continued revenue growth above the current baseline, Wisconsin has plenty of extra revenue to return to taxpayers in the form of permanent rate reductions and other structural improvements. As such, each of our sample comprehensive tax reform options would return approximately $1.2 billion of this revenue growth to taxpayers. Options A, B, and C would use sales tax base broadening and/or rate increases to offset the additional cost of income tax reductions above $1.2 billion, while Options D and E would each provide a sustainable net tax cut of approximately $1.2 billion without sales tax base broadening or rate increases, meaning the income tax cuts in Options D and E are smaller than in Options A, B, and C.

It is important to note, however, that rates could be dialed down even further if policymakers want to provide more than $1.2 billion in net tax relief, and rates could be dialed up slightly if policymakers want to dedicate less of the state’s revenue growth to tax relief.

Table 2 shows a summary of the provisions included in each comprehensive tax reform option, and Table 3 shows how the flat individual income tax rates in Options A through D could be dialed down or up depending on the amount of revenue growth lawmakers choose to return to taxpayers.

Detailed descriptions of each sample tax reform option are provided in the pages that follow.

| Net Tax Cut of $1.2 Billion | ||||||||

|---|---|---|---|---|---|---|---|---|

| Current Structure (Tax Year 2022) | Option A | Option B | Option C | Option D | Option E | |||

| Individual Income Tax | ||||||||

| Rate(s) | Single | MFJ | All filers | All filers | All filers | All filers | Single | MFJ |

| 3.54% > $0 | 3.54% > $0 | 4.15% | 4.5% | 4.5% | 5.1% | 3.3% > $0 | 3.3% > $0 | |

| 4.65% > $12,760 | 4.65% > $17,010 | 4.4% > $12,760 | 4.4% > 17,010 | |||||

| 5.30% > $25,520 | 5.30% > $34,030 | 5.0% > $25,520 | 5.0% > $34,030 | |||||

| 7.65% > $280,950 | 7.65% > $374,600 | 7.2% > $280,950 | 7.2% > $374,600 | |||||

| Enhanced standard deduction | √ | √ | √ | √ | √ | |||

| Corporate Income Tax | ||||||||

| Rate | 7.9% | 7% | 5.5% | 6.5% | 7.9% | 7% | ||

| Throwback rule repealed | √ | √ | √ | √ | ||||

| Economic development surcharge repealed | √ | √ | √ | √ | ||||

| Sales Tax | ||||||||

| Rate | 5% | 6% | 6% | 6% | 5% | 5% | ||

| Modest base broadening | √ | √ | ||||||

| Property Tax | ||||||||

| Personal property tax repealed | √ | √ | √ | √ | √ | |||

| Results of Proposed Changes | ||||||||

| State Business Tax Climate Index ranking | 27th | 8th | 8th | 9th | 9th | 21st | ||

|

Note: See text for description of enhanced standard deduction and Table 6 for components included in sales tax base broadening. The State Business Tax Climate Index ranking line shows what Wisconsin’s overall ranking on the 2022 Index would have been if sample options had been in effect on July 1, 2021. Sources: Tax Foundation calculations based on data from the Wisconsin Legislative Fiscal Bureau and the Wisconsin Department of Revenue. |

||||||||

| Net Tax Cut | Option A | Options B and C | Option D | |||||

|---|---|---|---|---|---|---|---|---|

| $1 billion | 4.30% | 4.60% | 5.20% | |||||

| $1.2 billion | 4.15% | 4.50% | 5.10% | |||||

| $1.4 billion | 4.00% | 4.40% | 5.00% | |||||

| $1.6 billion | 3.90% | 4.25% | 4.85% | |||||

| $2 billion | 3.80% | 4.10% | 4.70% | |||||

|

Note: See text for description of enhanced standard deduction and Table 6 for components included in sales tax base broadening. The State Business Tax Climate Index ranking line shows what Wisconsin’s overall ranking on the 2022 Index would have been if sample options had been in effect on July 1, 2021. Sources: Tax Foundation calculations based on data from the Wisconsin Legislative Fiscal Bureau and the Wisconsin Department of Revenue. |

||||||||

Option A

The primary goal of Option A is to create a more competitive individual income tax structure by consolidating four brackets into one and reducing the rate substantially, to a flat 4.15 percent. This option also includes a modest reduction to the corporate income tax rate, bringing it down nearly a percentage point, to 7 percent. To partially offset these reforms (above the $1.2 billion in assumed reductions against higher revenues), Option A would modestly broaden the sales tax base (see Table 6), while increasing the sales tax rate to 6 percent.

By adopting a single-rate individual income tax at a substantially lower rate, this approach would reduce Wisconsin’s overreliance on taxes on productivity, reducing the degree to which the tax code discourages additional investment and labor force participation. Modernizing the sales tax to include a wider range of consumption, particularly from higher earners, would inject progressivity into the sales tax while making it more neutral in its application to both goods and services. With a state sales tax rate of 6 percent, Wisconsin’s combined state and average local sales tax rate would be 6.43 percent, which would still be lower than the combined rates in 31 of the 45 states with statewide sales taxes.[8]

Option B

Option B prioritizes making both the individual and corporate income tax rates substantially more competitive, bringing the individual income tax rate to a flat 4.5 percent and the corporate income tax rate to 5.5 percent. To partially offset these reforms, Option B would modestly broaden the sales tax base while increasing the sales tax rate to 6 percent.

This option gives greater priority to enhancing the competitiveness of Wisconsin’s corporate income tax, a tax which falls on—and thus discourages—capital investment. Corporate income taxes are a small and declining share of state tax revenue across the country, as states acknowledge their disinducement to investment and confront the revenue volatility they add to state tax codes.

Option C

Option C’s individual income and sales tax rates are identical to those of Option B, but instead of achieving a substantially lower corporate income tax rate, Option C trims the corporate income tax rate to 6.5 percent while leaving the sales tax base unchanged.

Like Option B, by reducing both individual and corporate income taxes, Option C would make Wisconsin more attractive to all types of businesses, regardless of their legal structure. Even with a full percentage point increase in Wisconsin’s sales tax rate, the combined state and average local sales tax rate would still be lower than the rates in 31 of the 45 sales tax-levying states.

Option D

If policymakers want to achieve a flat individual income tax rate without offsetting sales tax rate or base changes, Option D presents one possible method for doing so. This option assumes Wisconsin’s general fund has grown enough in recent years to permanently return $1.2 billion to taxpayers. This is a conservative assumption, as the state is projected to end the FY 2021-23 biennium with a surplus of $3.8 billion,[9] and while the growth rate is likely to slow, general fund tax collections for FY 2022-23 are projected to exceed collections for FY 2021-22, just like FY 2021-22 collections exceeded FY 2020-21 collections.[10]

Option D achieves a flat individual income tax rate of 5.1 percent while making no changes to the corporate income tax or the sales tax.

Option E

If policymakers want to improve both Wisconsin’s individual and corporate income tax rates without relying on offsetting sales tax changes, Option E presents one way of doing so. Like Option D, Option E achieves a net tax cut of approximately $1.2 billion without increasing the sales tax rate or broadening the sales tax base. Option E trims the corporate income tax rate to 7 percent and trims each of Wisconsin’s four marginal individual income tax rates while retaining the current graduated-rate structure.

While this approach would not improve the state’s tax competitiveness as much as Options A through D would, Option E is nevertheless a step in the right direction and could be enacted along with tax triggers that dedicate a certain amount of future revenue growth to reducing the top marginal individual income tax rate, consolidating four brackets into one, and reducing the corporate income tax rate, similar to the ongoing reforms in Iowa.

A downside of this approach is that it would take longer for Wisconsin to achieve truly competitive income tax rates, but even so, making incremental improvements is far better than standing still as other states continue to outcompete Wisconsin. Several notable states, such as North Carolina, Indiana, and most recently Iowa, have made remarkable structural improvements by phasing in pro-growth reforms over time.

Tax Changes Included in All or Several Options

In addition to the provisions described above that are unique to each of the five sample comprehensive tax reform options, the following policy changes are included in all or several options, and their revenue effects were accounted for when calculating the amount by which rates could be reduced. Each of the following structural changes would make Wisconsin’s tax code simpler and more neutral.

Increase the Standard Deduction – Options A, B, C, D, and E

Wisconsin’s current sliding scale standard deduction is income-tested, with the amount taxpayers are eligible to claim decreasing as income increases. In tax year 2022, the maximum standard deduction a single filer can claim is $11,790. That amount phases down for single filers with Wisconsin income exceeding $16,990 and reaches zero for taxpayers with income exceeding $115,240.[11] The maximum standard deduction for married couples filing jointly is $21,820, and that amount phases down for those with income exceeding $24,520, phasing down to zero at $134,845 in Wisconsin income.

To provide targeted tax relief to those at the lower end of the income spectrum, all sample tax reform options increase both the maximum standard deduction and the amount of income at which the deduction phases down. Specifically, the single filer standard deduction and phaseout thresholds are each increased by $5,000, such that the maximum single filer deduction is $16,790, the phaseout begins at $21,990 in income, and the deduction phases out to zero at $120,240 in income. The standard deduction for other filers is increased by a proportionate amount as shown in Table 4.

| Single | MFJ | Head of Household | Married Filing Separately | |||||

|---|---|---|---|---|---|---|---|---|

| Current | Proposed | Current | Proposed | Current | Proposed | Current | Proposed | |

| Maximum deduction amount | $11,790 | $16,790 | $21,820 | $31,074 | $15,230 | $21,689 | $10,370 | $14,768 |

| Beginning of phasedown | $16,990 | $21,990 | $24,520 | $31,736 | $16,990 | $21,990 | $11,640 | $15,066 |

| Phaseout to zero | $115,240 | $120,240 | $134,845 | $140,696 | $115,240 | $120,240 | $64,072 | $66,852 |

|

Sources: Wisconsin Department of Revenue; Tax Foundation calculations. |

||||||||

Repeal the Economic Development Surcharge – Options A, B, C, and E

In addition to corporate or individual income tax liability, C corporations and S corporations with gross receipts of $4 million or more must pay an economic development surcharge.[12] For C corporations, the surcharge is 3 percent of Wisconsin gross tax liability, with a minimum tax of $25 and a maximum tax of $9,800. Revenue from this tax is earmarked to fund the Wisconsin Economic Development Corporation (WEDC). Compared to the current surcharge that is only levied on select businesses, the general fund would be a more neutral and stable source of revenue for the WEDC. As such, each of the options that reduce the corporate income tax rate also repeal the economic development surcharge and instead finance the WEDC through the general fund.

Repeal the Throwback Rule – Options A, B, C, and E

The throwback rule in Wisconsin’s corporate income tax code taxes the “nowhere income” of Wisconsin-based corporations. This reduces Wisconsin’s tax competitiveness, adds unnecessary complexity, and creates the potential for double taxation. Repealing the throwback rule would make Wisconsin more attractive to prospective employers, enhancing Wisconsin’s future growth prospects. Each of the options that reduce the corporate income tax rate also repeal the throwback rule (Options A, B, C, and E).

Repeal the Tangible Personal Property Tax – Options A, B, C, D, and E

While commendable progress has been made to reduce reliance on tangible personal property taxes over time, some property remains taxable, such as office furniture, fixtures, and equipment, as well as boats and other watercraft. Wisconsin policymakers have already set aside revenue to repeal this tax, but the tax will continue to be collected until lawmakers enact legislation removing it from the books.

Additional Tax Reform Considerations

Although not included in these plans, policymakers may also wish to reevaluate the married couple credit, which is designed to reduce—but not eliminate—the marriage penalty in Wisconsin’s tax code.

A flat individual income tax rate eliminates one of the two sources of the marriage penalty in Wisconsin’s tax code. The other contributor to the marriage penalty is the sliding scale standard deduction, which does not double for married filers. Based on data availability, our options scale up the standard deduction proportionately for all filers, maintaining progressivity in the tax code while implementing a single-rate tax. Given that the flat rates in Options A, B, C, and D will eliminate the marriage penalty in Wisconsin’s individual income tax brackets, policymakers could reduce the size of the married couple credit. Still better, policymakers could also explore eliminating the marriage penalty within the standard deduction, which would allow them to repeal the credit outright and provide greater equity for married filers than is available under the existing system.

Rebalancing Revenue Sources to Promote Economic Growth

When levying taxes to fund government services, some amount of economic drag is inevitable; this is a basic reality of taxation. But not all taxes are equal; some taxes are much more economically harmful and distortive than others. As such, tax structure matters greatly and can have a tremendous impact on a state’s economic well-being.

Policymakers often talk at length about how much revenue is raised, but the question of how that revenue is raised is just as important. Policymakers should always be on the lookout for ways to minimize economic harm and maintain a competitive, structurally sound tax code that allows all individuals and businesses the opportunity to thrive.

Economic research overwhelmingly finds corporate and individual income taxes to be more harmful to economic growth than well-structured sales and property taxes. Currently, however, compared to the nation as a whole, Wisconsin over-relies on more harmful taxes and under-relies on less harmful taxes.

Specifically, in fiscal year 2018-19, the most recent year of data available, 28.6 percent of Wisconsin’s state and local tax collections came from individual income taxes, compared to 24.1 percent of total state and local tax collections nationally. Similarly, Wisconsin generated 4.5 percent of state and local tax collections from its corporate income tax, compared to a national figure of 3.5 percent. But while 23.3 percent of total state and local tax collections nationwide came from general sales and use taxes, only 20.1 percent of Wisconsin’s collections came from that tax. Looking at state tax collections only, the individual income tax is far and away the largest revenue source, generating $8.7 billion, or 43.7 percent of state tax collections, in FY 2018-29, compared to only 28.4 percent generated by the general sales tax.

Aided by a strong budget surplus and projected continued revenue growth, Wisconsin has an opportunity to rebalance its tax structure—even without reducing government spending—to better promote long-term economic growth and opportunity in the Badger State. The following pages explain how various reforms proposed in the sample tax reform options would improve the state’s tax structure and competitiveness.

Corporate Income Taxes

Wisconsin’s Corporate Income Tax Rate Is Among the Highest in the Nation

While the profits of pass-through businesses are taxed at the individual level instead of the entity level, the profits of C corporations are double taxed. C corporations are taxed first at the entity level (where the corporate income tax rate is applied) and again at the shareholder level, when individual shareholders pay individual income taxes on dividends received.

As of July 1, 2022, Wisconsin’s corporate income tax rate of 7.9 percent is higher than the top rates in all but 12 states and the District of Columbia.[13] One of those 12 states—neighboring Iowa—is on track to grow substantially more competitive under recent reforms that will broaden the corporate income tax base while reducing the rate from 9.8 to 5.5 percent over time as specified revenue targets are met.[14]

Taxes matter to businesses, and numerous economic studies show corporate income taxes are among the most harmful to economic growth. In a comprehensive review of international econometric tax studies, Arnold et. al. (2011) found corporate income taxes to be the most detrimental to economic growth, followed by individual income taxes, while finding consumption and property taxes to be less economically harmful.[15] Among the major taxes levied by state and local governments, Harden and Hoyt (2002) found the corporate income tax has the most significant negative impact on the rate of growth in employment.[16] Newman (1982) found corporate income tax differentials to be a major factor influencing businesses’ moves to Southern states.[17] Agostini and Tulayasathien (2001) found a state’s corporate income tax rate to be the most relevant tax to foreign direct investors deciding where to invest.

Lower Income Tax Rates Reduce the Need for Business Tax Incentives

To attract certain forms of business investment despite high income tax rates, Wisconsin’s tax code offers special tax breaks for legacy industries like manufacturing and agriculture. Separately, policymakers have offered hefty tax incentives to lure specific firms to the state in exchange for their agreeing to meet certain investment and hiring targets. But Wisconsinites have seen firsthand how not all business investment and hiring goals pan out as desired, and how a great deal of deadweight loss can occur when government and business leaders rely too heavily on specific investments to drive job growth and economic opportunity in their state.

Furthermore, while incentives can substantially reduce and in some cases wipe out some forms of tax liability for some firms, they do nothing to help businesses in other sectors. This unequal treatment hinders diversified investment in Wisconsin, shifting a disproportionate share of the burden to non-qualifying firms.

If a state has to resort to large and frequent tax incentives to attract business investment, that is a sign of an uncompetitive underlying tax code. Instead of relying heavily on incentives to smooth the roughest edges of the tax code, a simpler, more efficient, and more neutral approach would be to create and maintain a tax code that avoids disincentivizing labor and investment in the first place, regardless of industry sector or how long a business has operated in the state.

Corporate Income Taxes Fall on Workers, Consumers, and Investors

It is also important to remember that while corporations are legally responsible for paying the corporate income tax, the economic burden of the corporate income tax falls on workers in the form of lower wages, on consumers in the form of higher prices, and on investors in the form of lower returns.[18] As such, everyone is affected by corporate income taxes, even if not aware of it.

Corporate Income Taxes Are a Volatile Source of Revenue

Another reason many states have reduced reliance on corporate income taxes in recent years is because they are a highly volatile revenue source. During economic contractions, nearly all revenue streams see collections decline, but property and sales tax collections can only decline so much, while business income can drop substantially, with businesses experiencing net losses rather than profits both during economic contractions and during ordinary business cycle fluctuations.

Relying on unstable revenue sources does a disservice not just to the state but also to those who rely on government programs, as revenue shortfalls may lead to budget cuts during periods of economic hardship. Policymakers should strive to maintain a tax system that minimizes economic harms while generating a stable source of revenue. Heavy reliance on corporate income taxes interferes with both objectives.

Reducing the Corporate Income Tax Rate Would Help Wisconsin Compete Regionally and Nationally

In an increasingly competitive environment, Wisconsin’s high corporate income tax rate is making the state an outlier. In 2021 alone, seven states enacted laws to reduce their corporate income tax rates: Arkansas, Idaho, Louisiana, Nebraska, New Hampshire, North Carolina, and Oklahoma. In 2022, Idaho, Nebraska, and New Hampshire enacted additional laws to reduce their rates even further, and Iowa and Utah joined the list of states enacting reductions. While many states have reduced their reliance on corporate taxes in recent years due to their revenue volatility and detrimental impact on business investment, not once since the enactment of Wisconsin’s corporate income tax in 1911 has the rate been reduced. If Wisconsin policymakers want to create a competitive tax code that minimizes economic harm, reducing the corporate income tax rate ought to be a priority.

Wisconsin’s Throwback Rule Hurts In-State Businesses

Several of our sample tax reform options propose repealing the throwback rule, another uncompetitive feature of Wisconsin’s corporate tax code. The throwback rule exposes income from Wisconsin-based outbound sales to Wisconsin’s high corporate income tax rate if that income is not taxable in the destination state. As of January 1, 2023, Wisconsin will be one of only 18 states plus the District of Columbia with a throwback rule, where “nowhere income” is included in the numerator of the sales factor of the apportionment formula (thereby treating “nowhere income” sales as if they had been made into Wisconsin). Two other states use a less aggressive throwout rule, where “nowhere income” is subtracted from the denominator of the sales factor of the apportionment formula, thereby excluding sales that generate “nowhere income” from the calculation of “sales made everywhere.”

Under federal laws governing interstate taxation, the income of a multistate corporation is apportioned among the states in which it operates to determine the share of the firm’s income each state has legal authority to tax (known as “nexus”). Generally, a state can tax a corporation’s income only when the corporation has some sort of physical presence, either property or employees, in the state. Each state has broad discretion, however, to establish its own apportionment formula based on some combination of the corporation’s property, payroll, and/or sales in the taxing state.

Under Wisconsin’s single sales factor apportionment formula, firms that have nexus in Wisconsin are subject to Wisconsin’s corporate income tax based solely on the sales they make into Wisconsin as a share of sales made into all states.[19] Unlike formulas that take property or payroll into account, single sales factor apportionment avoids directly increasing Wisconsin corporate income tax liability based on the extent to which a firm locates its facilities or employees in Wisconsin. This apportionment formula therefore tends to favor firms that have facilities or employees in Wisconsin but sell primarily into other states, as most states’ corporate income tax rates are lower than Wisconsin’s.

Efforts to mitigate in-state firms’ exposure to Wisconsin’s high corporate income tax rate through single sales factor apportionment are countered, however, by the state’s throwback rule, which substantially increases tax liability for Wisconsin-based firms that sell into states with which they have no nexus.

Given the prevalence of e-commerce in today’s economy, it is common for firms to make sales into states where they do not have property or employees. Similarly, many manufacturing businesses may have out-of-state customer bases—including retailers—who pick up merchandise in Wisconsin or otherwise facilitate sales that do not establish out-of-state nexus for a Wisconsin company. These sales generate “nowhere income,” income that is taxed by the federal government but is not taxable in any state. Wisconsin’s throwback rule requires in-state firms to report their nowhere income to Wisconsin so it can be “thrown back” into Wisconsin’s corporate income tax base and taxed at the 7.9 percent rate despite that income not being attributable to sales made into Wisconsin.

This can increase in-state corporate income tax liability to such an extent that some firms go out of their way to avoid originating sales from states with throwback rules.[20] In some cases, firms’ efforts to avoid exposure to throwback rules cost states more revenue on net than they gain from taxing nowhere income in the first place, given the extent to which firms avoid originating sales from states with throwback rules.[21] But not all businesses have the flexibility to plan their business activities around the tax code, so some firms are exposed to especially high effective state corporate income tax rates because of this rule.

Throwback rules were originally created to mitigate the perceived problem of less than 100 percent taxability of corporate income, but they instead create a complex system that can expose more than 100 percent of a firm’s income to taxation, while distorting business decisions and driving some firms out of state.[22] Given these negative effects, several states have repealed their throwback rules in recent years, including Missouri in 2020 and Alabama and West Virginia in 2021. Vermont’s 2022 repeal of its throwback rule will take effect January 1, 2023, and lawmakers in Louisiana are also seriously considering repeal.

Repealing Wisconsin’s throwback rule would result in a modest reduction in corporate income tax collections in the near term, but it would create a substantially more competitive environment in the long run, attracting new investment and promoting stronger economic and revenue growth over time. The surplus revenue Wisconsin has brought in in recent years can help offset temporary transition costs associated with repealing the throwback rule.

Individual Income Taxes

Wisconsin’s Individual Income Tax Rate Is Among the Highest in the Nation

As with corporate income taxes, Wisconsin relies especially heavily on individual income taxes. Wisconsin’s graduated-rate individual income tax structure has four brackets with a top marginal rate of 7.65 percent, higher than the top marginal rates in all but eight states and the District of Columbia.

High individual income tax rates reduce returns to labor, putting a damper on hours worked and workforce participation rates. High individual income tax rates also affect Wisconsin’s businesses, 95 percent of which are structured as pass-throughs, where business profits “pass through” to the owners’ individual income tax forms. In Wisconsin, sole proprietorships, partnerships, limited liability companies (LLCs), and S corporations are all taxed under the individual income tax code rather than the corporate income tax code. Approximately two-thirds of pass-through business income is exposed to the 7.65 percent rate. High tax rates mean business owners have less money to reinvest in their businesses, and this results in less hiring, less capital investment, and less economic output.

Recent Reductions to the Three Lowest Rates

In recent years, Wisconsin’s lower marginal individual income tax rates have been reduced on several occasions, with reductions occurring in 2019, 2020, and 2021 that have provided permanent tax relief to low- and middle-income taxpayers. These rate changes are shown in Table 5 and are described below.

| Tax Years 2018-2022 | |||||||

|---|---|---|---|---|---|---|---|

| Single | Married Filing Jointly | ||||||

| 2022 | |||||||

| 3.54% | > | $0 | 3.54% | > | $0 | ||

| 4.65% | > | $12,760 | 4.65% | > | $17,010 | ||

| 5.30% | > | $25,520 | 5.30% | > | $34,030 | ||

| 7.65% | > | $280,950 | 7.65% | > | $374,600 | ||

| 2021 | |||||||

| 3.54% | > | $0 | 3.54% | > | $0 | ||

| 4.65% | > | $12,120 | 4.65% | > | $16,160 | ||

| Rate reduction -> | 5.30% | > | $24,250 | 5.30% | > | $32,330 | |

| 7.65% | > | $266,930 | 7.65% | > | $355,910 | ||

| 2020 | |||||||

| Rate reduction -> | 3.54% | > | $0 | 3.54% | > | $0 | |

| Rate reduction -> | 4.65% | > | $11,970 | 4.65% | > | $15,960 | |

| 6.27% | > | $23,930 | 6.27% | > | $31,910 | ||

| 7.65% | > | $263,480 | 7.65% | > | $351,310 | ||

| 2019 | |||||||

| Rate reduction -> | 3.86% | > | $0 | 3.86% | > | $0 | |

| Rate reduction -> | 5.04% | > | $11,760 | 5.04% | > | $15,680 | |

| 6.27% | > | $23,520 | 6.27% | > | $31,360 | ||

| 7.65% | > | $258,950 | 7.65% | > | $345,270 | ||

| 2018 | |||||||

| 4.00% | > | $0 | 4.00% | > | $0 | ||

| 5.84% | > | $11,450 | 5.84% | > | $15,270 | ||

| 6.27% | > | $22,900 | 6.27% | > | $30,540 | ||

| 7.65% | > | $252,150 | 7.65% | > | $336,200 | ||

|

Source: Wisconsin Department of Revenue. |

|||||||

On July 3, 2019, Gov. Tony Evers (D) approved with partial vetoes A.B. 56 (Act 9), the biennial budget for fiscal years (FYs) 2019-21. One of the approved provisions was a reduction to Wisconsin’s second-lowest individual income tax rate, lowering it from 5.84 to 5.21 percent, retroactive to January 1, 2019.

A separate bill enacted that same day, A.B. 251 (Act 10), prescribed a reduction to Wisconsin’s first two marginal individual income tax rates to offset the influx in online sales tax revenue attributable to the state’s response to the U.S. Supreme Court’s decision in South Dakota v. Wayfair. Specifically, Act 10 directed the Wisconsin Department of Revenue to reduce the first two marginal rates for tax year 2019 based on the actual influx in sales tax collections between Oct. 1, 2018, and Sept. 30, 2019, that was attributable to increased collections from remote sellers post-Wayfair.

Act 10 further specified that for tax year 2020, the amount of actual Wayfair-related sales tax revenue collected between Oct. 1, 2019, and Sept. 30, 2020, would be used to determine the first two marginal rates for 2020, and that those 2020 rates would be permanent. As a result, the interaction between Act 9 and Act 10 resulted in Wisconsin’s two lowest rates being reduced in both 2019 and 2020. The lowest marginal rate was reduced from 4.0 to 3.86 to 3.54 percent, and the second-lowest rate was reduced from 5.84 to 5.04 to 4.65 percent.

Two years later, on July 8, 2021, the governor approved with partial vetoes A.B. 68 (Act 58), the biennial budget for FYs 2021-23. One of the approved provisions was a reduction to the second-highest individual income tax rate, lowering it from 6.27 to 5.3 percent. This change was effective retroactive to Jan. 1, 2021.

Prior to this reduction, Wisconsin’s second-highest individual income tax rate was higher than the top marginal rates in more than half the states that levy an individual income tax.[23] Most Wisconsin taxpayers benefited from this reduction, as it affected single filers with just over $24,000 in taxable income and married couples with just over $32,000 in taxable income.

The Importance of Reducing the Top Marginal Individual Income Tax Rate

Since 2019, the only rate that has been left unchanged, then, is the one that has the most detrimental impact on labor and investment in Wisconsin: the top marginal rate. Wisconsin’s top marginal rate has stood at 7.65 percent since 2013, when it was reduced slightly from 7.75 percent.[24] At 7.65 percent, Wisconsin’s top rate is higher than the top rates in all but eight states and the District of Columbia.[25] Soon, only seven states and D.C. will have a higher top rate, as Iowa’s top marginal rate is set to decrease from 8.53 percent in 2022 to 6 percent in 2023, with further reductions scheduled each year until a flat rate of 3.9 percent is achieved in 2026.[26] Iowa’s progress is especially remarkable given the top rate was 8.98 percent (with a state deduction for federal taxes paid) as recently as 2018.

From an economic growth standpoint, the top marginal rate is the most important rate for policymakers to reduce because it has a far greater negative impact on economic growth than do the lower marginal rates. Personal and business decisions about labor, relocation, and investment are made on the margin—that is, based on how taxes will affect the next dollar of income, not previous dollars of income. Under Wisconsin’s current system, the top marginal rate of 7.65 percent is 2.35 percentage points higher than the next-highest rate of 5.3 percent, meaning taxpayers with income exposed to the top rate see a significant reduction to the benefit they receive from engaging in additional work. When the marginal benefit of additional labor is reduced, taxpayers work fewer hours, and some withdraw from the workforce altogether. This reduces economic output over time.

Reductions to top marginal individual income tax rates have been shown to encourage productivity and promote long-term economic growth, while increases to top marginal rates hurt economic growth. In a study of state tax changes from 1969 to 1986, Mullen and Williams (1994) found higher marginal rates reduce gross state product growth, even after adjusting for overall state tax burdens.[27]

In a review of the economic literature surrounding graduated-rate individual income taxes, Tax Foundation’s Timothy Vermeer analyzes several studies showing reductions to income tax rates lead to increases in wages, hours worked, and economic output, as well as decreases in unemployment rates.[28]

Specifically, Mertens and Olea (2013, updated 2017) found marginal individual income tax rate reductions led to an increase in the aggregate number of hours worked due to the employment of those who had previously been unemployed and an increase in the number of hours worked by those already employed.[29] They also found a negative relationship between changes in income tax rates and the wages of both higher-income and lower-income workers. Further, the authors found non-wage income to be responsive to tax rate changes, including pass-through business income, rents, interest and dividend income, and realized capital gains. Mertens and Ravn (2013) found reductions in average individual income tax rates have a positive effect on real GDP per capita and led to increases in durable goods consumption and private sector investment.[30]

Mertens and Olea (2013, 2017) found a notable distinction between the effects on economic activity of reductions to average tax rates (defined as “federal personal current taxes and contributions for social insurance…divided by total market income”) and marginal tax rates. Specifically, they found reductions to marginal rates lead to nearly proportional increases in income even when the average tax rate remains unchanged. This study helps explain why reducing marginal tax rates—especially the top marginal rate—tends to be more economically beneficial than reducing income tax liability through other means, such as by carving out large portions of the tax base through various exemptions and credits. To individuals and businesses making labor and investment decisions, tax rates send a far more visible signal than base provisions as to the relative attractiveness of a state’s tax environment. For example, Iowa’s elimination of its state deduction for federal taxes paid is freeing up revenue for the state to reduce rates dramatically, which will reduce the “sticker shock” to prospective taxpayers of the tax costs of working or doing business in Iowa.

When considering reductions to Wisconsin’s top marginal individual income tax rate, it is important to keep in mind that Wisconsin’s high top rate directly affects more than just the wealthy; it affects Wisconsin’s small businesses as well. Approximately 95 percent of all businesses in Wisconsin are structured as pass-throughs, where business income is taxed under the individual income tax code rather than the corporate income tax code.[31]

Many people think of pass-through businesses as small businesses, but most C corporations are small businesses as well. In fact, 99 percent of all Wisconsin businesses—including pass-throughs as well as C corporations—meet the U.S. Small Business Administration’s definition of a small business.[32]

In tax year 2019, 75 percent of Wisconsin pass-through business income was reported on tax returns with more than $200,000 in adjusted gross income (AGI), and 55 percent of Wisconsin pass-through business income was reported on returns with more than $500,000 in AGI.[33] Under Wisconsin’s rate schedules (for single, joint, and head of household filers), we estimate that 67 percent of pass-through business income is subject to the top marginal rate, a high 7.65 percent tax on entrepreneurial activity.

Reductions to Wisconsin’s top marginal individual income tax rate would be a game changer for many of the state’s small businesses, yielding positive effects on entrepreneurship, business investment, and job growth for years to come.

Economic research also shows the benefits of reductions to the top rate affect more than just those whose income tax liability is directly reduced. Those rate reductions benefit those with lower incomes, as well, through positive effects on wages, employment, and overall economic conditions. Mertens and Olea (2013, updated 2017) found a cut to the average marginal tax rate that applies only to the top 1 percent of the income distribution would increase real GDP, reduce unemployment, and have a positive effect on the incomes of those not in the top 1 percent of the income distribution.[34]

While reducing Wisconsin’s top marginal individual income tax rate would yield benefits for the state and its taxpayers, an even better option would be for the state to consolidate its four brackets into one while dedicating future revenue growth to rate reductions over time. The following section highlights the benefits of moving from a graduated-rate to a single-rate individual income tax structure.

States are Trending Toward Flat Taxes

In 1912, Wisconsin became the first state to implement a workable income tax after many states had tried and failed. First collected in 1912 based on 1911 income,[35] Wisconsin’s individual income tax originally had 13 brackets and a top rate of 6 percent.[36] Five years later, Massachusetts implemented the nation’s first single-rate individual income tax.[37]

While many states made changes to their rates and brackets in the decades to follow, no state converted its graduated-rate tax into a single-rate structure until 75 years of state income taxation had passed and all the broad-based state individual income taxes that currently exist already had been enacted.[38]

In 1987, Colorado became the first and only state during the 20th century to shift from a graduated-rate to a single-rate structure. It was followed by Utah in 2007, North Carolina in 2014, and Kentucky in 2019. While it took more than a century for the first four states to make that shift, 2022 alone brought a wave of four more states enacting laws or receiving court clearance to make that transition.[39]

Specifically, Iowa policymakers enacted a law to phase in a flat rate of 3.9 percent by 2026. Mississippi will have a flat rate of 5 percent in 2023, which is scheduled to be reduced to 4 percent by 2026. Georgia will have a flat rate of 5.49 percent in 2024, and the rate is scheduled to phase down to 4.99 percent over time. Finally, a court in Arizona cleared the path for the implementation of a 2021 law that, contingent upon revenue meeting specified targets, will phase in a flat tax at a rate of 2.5 percent as early as 2024.[40] Oklahoma is another state that gave serious consideration to flat tax legislation in 2022.

A Flat Tax Structure Would Benefit Wisconsin and Its Taxpayers

Moving to a single-rate structure would yield many benefits for Wisconsin and its taxpayers, the most notable being that single-rate structures are better than graduated-rate structures at promoting growth-inducing economic activities. Wisconsin’s current graduated-rate structure imposes steep penalties on additional labor and investment on the margin, reducing the value to Wisconsinites of working additional hours, finding a higher-paying job, or making additional income-generating investments. Alternatively, under a flat tax structure, Wisconsinites would bring home the same amount of income for every dollar of taxable income earned, whether their first dollar of taxable income, their latest dollar of income, or any future dollars of income. This approach is far more neutral and pro-growth, and it creates an environment that is much friendlier to innovation and upward mobility.

The economic literature on progressive tax structures shows they have a negative effect on upward mobility and wage growth. Gentry and Hubbard (2002) found a statistically significant relationship between decreases in the progressivity of individual income tax structures and the probability of workers transitioning to a better job within a year.[41] They also found a statistically significant negative relationship between tax progressivity and the real growth rate of wages.

In addition to the economic benefits, single-rate structures better embody the principles of sound tax policy, including simplicity, transparency, and neutrality. Because all income-tax payers would be affected by a rate change, policymakers would likely work harder to justify any proposed rate increase, as it would affect a larger share of their constituents. Over time, this can help stave off unnecessary tax increases and promote the more efficient stewardship of taxpayers’ resources.

Taxpayers seem to recognize this intuitively. In November 2020, Illinois voters soundly rejected a proposed constitutional amendment that would have permitted a graduated-rate structure even though the initial rates proactively passed by the General Assembly would have kept them at or below 4.95 percent for the first $250,000 in taxable income.[42] Voters seemed to understand that if a graduated-rate structure were adopted, future rate increases would become more likely.[43]

Flat taxes are also simpler and better enhance government transparency. Under a single-rate structure, taxpayers can quickly estimate their effective state income tax rate without so much as a calculator, and they can more easily estimate the extent to which a proposed rate change would affect them. Under a graduated-rate structure, however, effective tax rates are more easily disguised. Very few taxpayers have the tax rates and brackets memorized, and many, if asked, would not be able to name the rate to which their top dollar of income is exposed.

For state revenue forecasters, policymakers, and other stakeholders, a single-rate structure would also make it easier to forecast future revenue changes based on economic conditions, as well as to estimate how proposed tax policy changes would impact state revenue in the aggregate and individual taxpayers on a more granular level.

Proponents of graduated-rate income tax systems tend to view them as a way to address income inequality, but research—including a study by Feldstein and Wrobel (1998)—shows that higher marginal rates lead to a relocation of capital and higher earners to more favorable tax environments.[44] This not only undercuts the state’s efforts to expose high earners to higher taxes, but also reduces the income of lower-income individuals who remain, due to reduced opportunities and a less competitive economic environment.

It is worth noting that even with a single-rate structure, Wisconsin’s income tax code would contain elements of progressivity through various deductions, exemptions, and credits that exclude certain income from taxation altogether or reduce effective rates for lower-income taxpayers. These provisions include the standard deduction, as well as the refundable earned income credit and refundable homestead credit.

It is also important to remember that when it comes to questions of progressivity and equity, taxes tell only one side of the story. Even with a less progressive income tax structure, Wisconsin’s tax and transfer system would continue to be progressive, given state and local spending on food and nutrition assistance programs like SNAP and WIC; affordable housing; health care, childcare, and utilities payment assistance; vocational education and training; and other income-tested programs providing financial support to lower-income individuals and families. The tax code is not always—or even often—the best way to provide income supports or other varieties of low-income assistance.

Currently, nine states have flat individual income tax structures, with five of those states adding another layer of protection to that status by making a flat tax structure part of their state constitutions. An additional four states have enacted laws to transition to a flat tax, for a total of 13 states that have, or are in the process of implementing, a single-rate structure.[45] Four of those states—Iowa, Illinois, Indiana, and Michigan—border Wisconsin. An additional five states—Alabama, Arkansas, Idaho, Missouri, and Oklahoma—have structures that technically are graduated but effectively are close to flat, with top rates kicking in at or below $10,000 in taxable income.

Triggers Could Continue the Work of Reform

Across the country, revenue triggers have emerged as an effective way to implement or phase in tax rate reductions or other tax reform measures as revenues permit. Tax triggers are a newer take on an old concept: contingent enactment of a legislative provision. States have long relied upon bills with contingent enactment clauses, providing that certain features of new legislation shall only be operative if certain conditions are met. Tax triggers build on this model, making tax reform measures contingent on state revenues meeting or exceeding established targets.[46]

Tax triggers can help ensure revenue stability and limit the uncertainty associated with changes to the tax code while providing an efficient way for states to dedicate some portion of revenue growth to tax relief. Their ability to do so, however, depends on their design. Poorly designed triggers can implement cuts when economic conditions do not warrant it or postpone reductions even when revenue growth would permit it. By contrast, properly constructed tax triggers are a valuable mechanism for providing meaningful rate relief.

Well-designed triggers require selecting a baseline revenue figure—either a given year’s revenue or a statutorily established amount—and then establishing benchmarks that reflect meaningful revenue growth. Lawmakers should not use year-over-year revenue changes but instead establish a specific revenue baseline and employ benchmarks that measure real revenue growth, adjusted for inflation, over that base year amount. Ideally, reductions should not be tied to specific years but instead triggered whenever real revenue growth is adequate to reduce rates by at least a given increment—say 10 or 25 basis points—with the actual size of the reduction based on a statutorily established proportion of inflation-adjusted revenue growth.

Sales Taxes

Wisconsin’s Sales Tax Rate Is Among the Lowest in the Nation

While Wisconsin’s individual and corporate income tax rates are high compared to the rest of the country, its sales tax rate is among the lowest in the nation. At 5 percent, Wisconsin’s state sales tax rate is well below average, and the combined state and average local sales tax rate of 5.43 percent is the third lowest in the country behind only Wyoming (5.22 percent) and Alaska, which has an average local sales tax rate of 1.76 percent but does not have a state-level sales tax.

Wisconsin’s Sales Tax Base Has Room for Modernization

Wisconsin’s sales tax base, the basket of goods and services to which the sales tax applies, is slightly broader than the national median, but many notable categories of consumer goods and services remain exempt that ought to be taxed. While comparing states’ sales tax breadth is challenging because each state taxes a unique set of goods and services, one way to approximate sales tax breadth is to calculate the total value of taxed transactions as a percentage of total state personal income. In Wisconsin, this yields a sales tax breadth of 36.92 percent, slightly higher than the national median of 35.72 percent.[47]

Sales Taxes Are Less Economically Harmful Than Income Taxes

The economic literature on consumption taxes consistently finds they are less harmful than income taxes, especially when the sales tax is destination-based, as Wisconsin’s is, and when the tax is applied to final retail consumption only, not business-to-business purchases.[48]

In a study examining the economic effects of income and consumption taxes in the United Kingdom, Nguyen, Onnis, and Rossi (2021) found income tax changes had large and persistent effects on income, consumption, and investment, while consumption taxes had only modest effects.[49] In a study on public spending, taxation, and long-term economic growth, Bleaney, Gemmell, and Kneller (2001) conclude that consumption taxes do not cause economic distortions.[50] Economists affiliated with the Organisation for Economic Co-operation and Development (OECD) found that a 1 percent shift of tax revenues away from income taxes toward consumption and property taxes would increase long-run GDP per capita by as much as 1 percent.[51] Additionally, a Canadian study found sales tax increases to be associated with increases in economic growth due to sales taxes often replacing taxes on income and investment.[52]

A key reason sales taxes are less economically harmful is because they apply to present consumption only, whereas income taxes apply both to income that is consumed now and to income that is saved or invested to be spent later, which leads to double taxation of consumption when sales taxes are also applied.[53]

Because consumption taxes are less harmful to economic growth than are income taxes, lawmakers should consider increasing reliance on the sales tax to reduce reliance on more harmful corporate and individual income taxes. Tennessee is one example of a state that is enjoying robust economic growth and strong net inbound migration despite its high sales tax rate and larger-than-average sales tax base, as this heavy reliance on consumption taxes enables the state to completely forgo individual income taxes.

Increased Sales Tax Reliance Can Offset Income Tax Rate Reductions

Because consumption is a more neutral and less harmful tax base than income, several of the sample comprehensive tax reform options proposed in this report increase reliance on sales taxes to partially offset individual and corporate income tax rate reductions and reforms.

Policymakers can use sales tax base broadening, sales tax rate increases, or both, to offset income tax rate reductions, but of those two options, base broadening ideally would be considered first, as economists generally agree that broad-based, low-rate taxes are structurally superior to narrow-based, high-rate taxes, as they are more neutral and generate a more stable source of revenue.

Specifically, Wisconsin’s sales tax base could be expanded to a variety of consumer services that have never been taxed, as well as to various consumer goods that were carved out of the sales tax base over time. Sales taxes should not, however, be newly applied to business-to-business transactions. Taxing business inputs leads to tax pyramiding, where taxes often get embedded in the prices of final goods and services multiple times over and in a nontransparent manner. Taxing business-to-business purchases is also nonneutral in that it harms some industries more than others and encourages vertical integration of supply chains to avoid the tax.

Table 6 shows a list of some of the currently untaxed consumer services and goods that could be included in the sales tax base to generate revenue to offset income tax reforms. Using data from the Wisconsin Department of Revenue’s 2021 Summary of Tax Exemption Devices and the Wisconsin Legislative Fiscal Bureau’s January 2022 revenues forecasts, we estimate broadening the sales tax base to the household consumption (not business-to-business purchases) of the following services would increase revenue by approximately $291 million in FY 2022-23.[54]

It is also important to keep in mind that because Wisconsin has a uniform state and local sales tax base, any expansion of the state sales tax base would extend to the local base as well, yielding increased revenue for counties.

| Consumer Good or Service | Estimated Fiscal Effect (FY 2022-23) |

|---|---|

| Repair of Real Property | $72,467,355 |

| Beauty, Barber, Nail and Other Personal Care Services | $56,233,428 |

| Veterinary Services for Pets | $39,516,387 |

| Accounting Services* | $21,590,317 |

| Health Clubs | $20,439,510 |

| Funeral Services, excluding Caskets and Vaults | $16,970,987 |

| Dues and Fees Paid to Business Associations and Fraternal Organizations | $16,351,608 |

| Newspapers, Periodicals, and Shoppers Guides | $13,378,589 |

| Admissions to Educational Events and Places | $10,157,817 |

| Disinfecting and Exterminating | $7,184,798 |

| Interior Design* | $3,096,896 |

| Caskets and Burial Vaults | $5,822,164 |

| Auto and Travel Clubs | $4,707,281 |

| Tax Preparation Services* | $3,406,585 |

| TOTAL | $291,323,720 |

|

Note: The estimated fiscal effects for accounting, interior design, and tax preparation services assume the sales tax is applied only when those services are purchased by individuals, not businesses. Sources: Wisconsin Department of Revenue, “State of Wisconsin Tax Exemption Devices, 2021-23″; Wisconsin Legislative Fiscal Bureau, “Revenue Estimates January 25, 2022”; Council on State Taxation, “Sales Taxation of Business Inputs”; author’s calculations. |

|

Broadening the sales tax base would generate additional revenue while minimizing economic harms and making the tax code more neutral in the process.

Extending the sales tax to consumer services would also capture a larger share of personal consumption expenditures that tend to be more discretionary in nature and therefore are more often purchased by higher-income consumers. This would right an accidental wrong in the tax code that currently favors higher-income consumers by leaving many of their discretionary purchases untaxed.

In addition to broadening the sales tax base, policymakers could consider raising the sales tax rate. On a static basis and assuming no other economic effects, each percentage point of Wisconsin’s current 5 percent state sales tax generates approximately $1.45 billion, for a total of $7.23 billion in sales and use tax revenue expected to be collected in FY 2022-23.[55]

Large sales tax rate differentials among neighboring states can lead to cross-border shopping, but all of Wisconsin’s immediate neighbors have state and average local sales tax rates in the 6 to 8 percent range, leaving plenty of room for Wisconsin to raise sales tax rates while still maintaining a rate at or below the levels of its neighbors.[56]

Property Taxes

Real Property Taxes Are a Good Local Tax Base

Like its sales tax system, Wisconsin’s property tax system is relatively well structured in that its property taxes are simple and neutral in their application across different types of real property. As Wisconsinites are well aware, property taxes are indeed high in Wisconsin; homeowners face an effective property tax rate of 1.63 percent when considering property tax collections as a share of owner-occupied home value.[57] But real property is the least economically harmful of the major tax bases, so real property taxes are an appropriate source of local revenue to fund local government services.

Unlike labor or capital, real property is immobile, so tax avoidance options are limited. Real property taxes are also highly transparent and adhere well to the benefit principle in public finance that says taxes paid should relate closely with benefits received.

It is also important to note that heavier reliance on local real property taxes has enabled Wisconsin to keep the county local option sales tax rate much lower than the rates in most other states. Wisconsin counties have the option to levy a local sales tax at a rate of 0.5 percent, while the average local sales tax rate nationwide is roughly 2 percent.[58]

As a taxpayer protection mechanism, property taxes levied by Wisconsin school districts and municipal and county governments are subject to strict levy limits that essentially only permit collections to rise with voter approval.[59] These property tax caps have been effective in reducing overall property tax burdens in recent years, and they should be allowed to continue working.

The Personal Property Tax Remains Ripe for Elimination

This publication prioritizes discussion of income tax rates and related provisions that are most hindering Wisconsin’s economic competitiveness, but in the course of any tax reform conversations, one area of the property tax code that policymakers should prioritize for elimination is the counterproductive tax on business (and select other) personal property, sometimes known as the tangible personal property tax.

Wisconsin has already made commendable progress in exempting large categories of tangible property from ad valorem taxes over time, but annual property taxes continue to be collected on the value of office furniture, fixtures, and equipment; boats and other watercraft; and certain other items.[60]

Personal property taxes not only increase the cost of investing in Wisconsin, but they also impose substantial compliance costs, as businesses must proactively calculate the depreciable value of their taxable tangible personal property each year and remit the appropriate tax. In some cases, taxpayers expend more resources complying with this tax than they remit in tax liability, making it more of a nuisance tax than anything, and one that creates significant deadweight losses.

Since Wisconsin’s property taxes are exclusively a local levy, the elimination of the personal property tax would result in reduced tax revenue for local governments. To hold local governments harmless, state policymakers could simply increase their aid to localities based on a formula that takes the current value of taxable tangible property into account and adjusts for inflation.

An approach similar to this was considered during the 2021 legislative session, when the General Assembly sent a bill to the governor (A.B. 191) to repeal the personal property tax and appropriated funds in the budget to offset associated local revenue losses. Gov. Evers vetoed the personal property tax repeal legislation but did not veto the appropriation that went along with it. He then backed a separate bill (A.B. 641) to repeal the tax, but that legislation did not pass the General Assembly. Given that the General Assembly has already set aside revenue to offset local revenue losses, reaching an agreement to repeal the tax should remain a near-term priority.

Conclusion

While Wisconsin has made modest improvements to its individual income tax rates in recent years, the top marginal rate, the rate that matters most to the state’s economic competitiveness, remains among the highest in the country. Wisconsin’s corporate income tax rate is even higher, and these taxes on productivity are hurting the state’s ability to attract businesses and workers to the state. Our sample comprehensive tax reform options present five ways the Badger State’s tax code could be rebalanced to promote economic growth and competitiveness. Two of these reform options simply dedicate a portion of revenue growth to tax reform, while three of the options facilitate further income tax reductions by shifting additional reliance onto the sales tax, which currently has among the lowest rates in the country. Given the state’s strong budget surplus and projected continued revenue growth, Wisconsin is in a prime position to enact pro-growth reforms to improve the state’s competitive standing for decades to come.

[1] Jared Walczak, “Two Dozen States Show Why the Kansas Critique of Income Tax Cuts Is Mistaken,” Tax Foundation, May 24, 2022, https://www.taxfoundation.org/kansas-experiment-kansas-tax-cuts-critique/.

[2] Jared Walczak, “Iowa Enacts Sweeping Tax Reform,” Tax Foundation, Mar. 14, 2022, https://www.taxfoundation.org/iowa-tax-reform/.

[3] Timothy Vermeer and Katherine Loughead, “State Individual Income Tax Rates and Brackets for 2022,” Tax Foundation, Feb. 15, 2022, https://www.taxfoundation.org/publications/state-individual-income-tax-rates-and-brackets/.

[4] Katherine Loughead, Jared Walczak, and Joseph Bishop-Henchman, “Wisconsin Tax Options: A Guide to Fair, Simple, Pro-Growth Reform,” Tax Foundation, Feb. 13, 2019, 40, https://www.taxfoundation.org/wisconsin-tax-reform/.

[5] Janelle Fritts and Jared Walczak, 2022 State Business Tax Climate Index, Tax Foundation, Dec. 16, 2021, https://www.taxfoundation.org/2022-state-business-tax-climate-index/.

[6] Some 2019 rankings referenced here differ from rankings as originally published in the 2019 Index due to enactment of retroactive statutes and backcasting of methodological changes.

[7] Deneen Smith, “State Expects $3.8 Billion Surplus,” Wisconsin Public Radio, Apr. 26, 2022, https://www.urbanmilwaukee.com/2022/04/26/state-expects-3-8-billion-surplus/.

[8] Janelle Fritts, “State and Local Sales Tax Rates, 2022,” Tax Foundation, Feb. 3, 2022, https://www.taxfoundation.org/publications/state-and-local-sales-tax-rates/.

[9] Deneen Smith, “State Expects $3.8 Billion Surplus.”

[10] Wisconsin Department of Revenue, “Wisconsin Economic Forecast Update: February 2022,” https://www.revenue.wi.gov/dorreports/2022-02-wi-forecast.pdf.

[11] Wisconsin Department of Revenue, “Form 1 Instructions,” https://www.revenue.wi.gov/TaxForms2021/2021-Form1-Inst.pdf.

[12] Wisconsin Department of Revenue, “Economic Development Surcharge,” accessed June 15, 2022, https://www.revenue.wi.gov/Pages/FAQS/pcs-temp.aspx#rec1.

[13] Janelle Fritts, “State Corporate Income Tax Rates and Brackets for 2022,” Tax Foundation, Jan. 18, 2022, https://www.taxfoundation.org/publications/state-corporate-income-tax-rates-and-brackets/.

[14] Jared Walczak, “Iowa Enacts Sweeping Tax Reform.”

[15] Jens Arnold, Bert Brys, Christopher Heady, Åsa Johannsson, Cyrille Schwellnus, and Laura Vartia, “Tax Policy for Economic Recovery and Growth,” The Economic Journal 121:550 (February 2011).

[16] J. William Harden and William H. Hoyt, “Do States Choose their Mix of Taxes to Minimize Employment Losses?” National Tax Journal 56 (March 2003), 7-26.

[17] Robert J. Newman, “Industry Migration and Growth in the South,” The Review of Economics and Statistics 65:1 (February 1983), 76-86.

[18] Erica York, “New OECD Study Quantifies Crucial Role of Businesses in the Tax System,” Tax Foundation, Jan. 9, 2018, https://www.taxfoundation.org/oecd-study-quantifies-business-role-tax-system/.

[19] For some interstate firms, like pipelines and telecommunications companies, Wisconsin includes property or payroll factors in the apportionment formula.

[20] Vernon B. Savoie and Michael L. Burr, “The Throwback Rule: Concepts, Components, and Planning Opportunities,” Journal of State Taxation 2:19 (1983-1984), 33.

[21] Jared Walczak, “Throwback and Throwout Rules: A Primer,” Tax Foundation, July 2, 2019, 15, https://www.taxfoundation.org/state-throwback-rules-throwout-rules/.

[22] Jared Walczak, “Throwback and Throwout Rules: A Primer,” 16.

[23] Timothy Vermeer and Katherine Loughead, “State Individual Income Tax Rates and Brackets for 2022.”

[24] Dan Spika, “Individual Income Tax: Informational Paper #2,” Wisconsin Legislative Fiscal Bureau, January 2021, 31, https://docs.legis.wisconsin.gov/misc/lfb/informational_papers/january_2021/0002_individual_income_tax_informational_paper_2.pdf.

[25] Timothy Vermeer and Katherine Loughead, “State Individual Income Tax Rates and Brackets for 2022.”

[26] Jared Walczak, “Iowa Enacts Sweeping Tax Reform.”

[27] John K. Mullen and Martin Williams, “Marginal Tax Rates and State Economic Growth,” Regional Science and Urban Economics 24:6 (December 1994).

[28] Timothy Vermeer, “The Impact of Individual Income Tax Changes on Economic Growth,” Tax Foundation, June 14, 2022, https://www.taxfoundation.org/income-taxes-affect-economy/.

[29] Karel Mertens and Jose L. Montiel Olea, “Marginal Tax Rates and Income: New Time Series Evidence,” Quarterly Journal of Economics 133:4 (2018), 1803-1884.

[30] Karel Mertens and Morten O. Ravn, “The Dynamic Effects of Personal and Corporate Income Tax Changes in the United States,” American Economic Review 103:4 (2013), 1212-47.

[31] Internal Revenue Service, “SOI Tax Stats – State Data FY 2021,” https://www.irs.gov/statistics/soi-tax-stats-state-data-fy-2021, and “SOI Tax Stats – Historic Table 2,” Tax Year 2019, https://www.irs.gov/statistics/soi-tax-stats-historic-table-2.

[32] U.S. Small Business Administration Office of Advocacy, “2021 Small Business Profile: Wisconsin,” https://cdn.advocacy.sba.gov/wp-content/uploads/2021/08/30143729/Small-Business-Economic-Profile-WI.pdf.

[33] Internal Revenue Service, “Individual Income and Tax Data, by State and Size of Adjusted Gross Income,” Statistics of Income, Tax Year 2019, https://www.irs.gov/statistics/soi-tax-stats-historic-table-2.

[34] Karel Mertens and Jose L. Montiel Olea, “Marginal Tax Rates and Income: New Time Series Evidence,” 1803-1884.

[35] Kossuth Kent Kennan, “The Wisconsin Income Tax,” The Annals of the American Academy of Political and Social Science 58 (March 1915), 65-76, http://www.jstor.org/stable/1012848.

[36] Wisconsin Department of Revenue, “Wisconsin Individual Income Tax: A Primer Prepared for Wisconsin Legislative Council Symposia Series on State Income Tax Reform Information,” https://docs.legis.wisconsin.gov/misc/lc/study/2012/symposia_series_on_state_income_tax_reform_information/020_july_25_2012_meeting/july25koskinen.

[37] Jared Walczak, “States Inaugurate a Flat Tax Revolution,” Tax Foundation, Apr. 26, 2022, https://www.taxfoundation.org/flat-tax-state-income-tax-reform/.

[38] Scott Drenkard and Richard Borean, “When Did Your State Adopt Its Income Tax?” Tax Foundation, June 10, 2014, https://www.taxfoundation.org/when-did-your-state-adopt-its-income-tax.

[39] Jared Walczak, “States Inaugurate a Flat Tax Revolution.”

[40] Timothy Vermeer, “The Aftermath of Arizona’s Proposition 208 and the Potential for a Flat Tax,” Tax Foundation, Apr. 29, 2022, https://www.taxfoundation.org/arizona-flat-tax/, and Katherine Loughead, “What’s in Arizona’s Tax Reform Package?” Tax Foundation, July 1, 2021, https://www.taxfoundation.org/arizona-tax-reform/.

[41] William M. Gentry and R. Glenn Hubbard, “The Effects Of Progressive Income Taxation On Job Turnover,” Journal of Public Economics 88:9 (2002), 2301-2322.

[42] Jared Walczak and Katherine Loughead, “Twelve Things to Know About the ‘Fair Tax for Illinois,’” Tax Foundation, Oct. 6, 2020, 3, https://www.taxfoundation.org/illinois-fair-tax/.

[43] Jared Walczak, “States Inaugurate a Flat Tax Revolution.”

[44] Martin Feldstein and Marian V. Wrobel, “Can State Taxes Redistribute Income?” Journal of Public Economics 68:3 (1998), 369-96.

[45] Jared Walczak, “States Inaugurate a Flat Tax Revolution.”

[46] Jared Walczak, “Designing Tax Triggers: Lessons from the States,” Tax Foundation, Sept. 7, 2016, https://www.taxfoundation.org/designing-tax-triggers-lessons-states/.

[47] Jared Walczak, “State Sales Tax Breadth and Reliance, Fiscal Year 2021,” Tax Foundation, May 4, 2022, https://www.taxfoundation.org/state-sales-tax-base-reliance/.

[48] William McBride, “What Is the Evidence on Taxes and Growth?” Tax Foundation, Dec. 18, 2012, https://www.taxfoundation.org/what-evidence-taxes-and-growth/.

[49] Anh D. M. Nguyen, Luisanna Onnis, and Raffaele Rossi, “The Macroeconomic Effects of Income and Consumption Tax Changes,” American Economic Journal: Economic Policy 13:2 (2021), 439-66.